Mic Drop

Terravest FY2025 Review

///

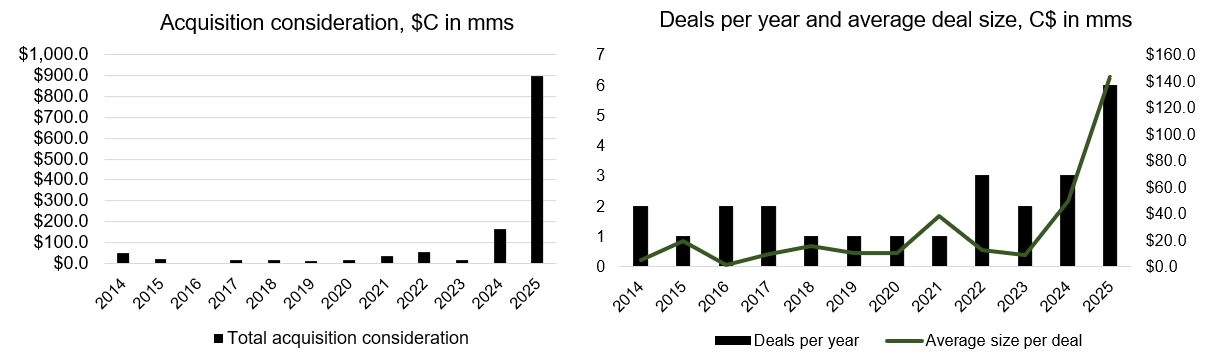

Whether Terravest’s acquisition program could scale was a reasonable question to ask last year, the 11th under Terravest’s current leadership. During those 11 years, Terravest completed 19 deals for total consideration of C$433 million including C$330 million in cash. Nearly half of that spend was in FY2024, when Terravest bought Highland Tank for just over C$100 million. The Highland Tank acquisition was roughly three times larger than Terravest’s next largest deal to date. To deploy 100% of its cash from operations on acquisitions in FY2024, Terravest needed a deal three times bigger than their previous largest deal and two other deal about as big as their largest deals historically; Highland Tank, Advanced Engineering Products, and LV Energy services, respectively. Whether Terravest’s acquisition program would continue to scale was a reasonable question to ask.

Terravest heard that and took it personally. In their FY2025, Terravest spent over C$850 million acquiring four businesses. One of those deals was their March 2025 C$780 million acquisition of Entrans. The Entrans deal alone is about double the size of all of the deals Terravest’s current leadership team has acquired while working together. Excluding Entrans, the amount Terravest spent on the other three deals in FY2025 would rank only behind FY2024 as Terravest’s most active in terms of acquisition spend. What we think of the deals, their future prospects, and Terravest’s ability to deploy capital going forward are all questions that I will address. But Terravest answered the question in 2025, in a big way.

I’ve owned Terravest for almost three years now. It’s a large position for me. I initially bought shares in March 2023 as a five percent position. After mulling it over for a few months, I doubled down in October 2023. So far, my analysis has been correct and my timing was lucky, initially. My goal in this write-up is to revisit my thesis and update a handful of numbers as well as my thoughts on Terravest.

Acquisitions and commentary.

Segment results and financial metrics.

Debt and equity details, insider sales.

Cash-on-cash returns and 11 year report card.

DCF, multiples and buying (supposedly) dying businesses.

Closing thoughts.

I start with a review of Terravest’s acquisition program. After that, I review segment results and a handful of financial metrics at the company level. Next I look at Terravest’s use of debt and equity, including the 2032 options and insider transactions. Then I take a step back and look at cash-on-cash returns and results over the past 11 years, spanning the current leadership’s tenure. My last exhibits are valuation related, a DCF, a few multiples and an updated decline model, which forecasts various return outcomes from buying supposedly dying businesses. I end with two closing thoughts, about owning those supposedly dying businesses and about pattern recognition.

Programming notes: Terravest’s fiscal years end on September 30th, references to years are to Terravest’s fiscal years, not calendar years. Terravest reports in Canadian dollars, all dollars referenced are Canadian dollars unless otherwise specified. A less straightforward programming note, more a question, is when to ‘start the clock’ on this leadership term’s tenure? Gilbert joined in 2013. In 2014, Terravest issued equity at cheap multiples three times, once as a secondary offering and twice relating to acquisitions, one of which brought in Charles Pellerin, who has served as Terravest’s executive chairman since. Including the 2014 is unflattering because of the equity issuances. We can see that those were uncharacteristic based on The Company’s net share reduction from 2015 - 2021. It doesn’t change the story much, and certainly not Terravest’s go-forward prospects, but something to consider. I include the 2014 deals and equity issuances throughout my analysis, for what it’s worth. Let’s get into them.

1. Acquisitions and commentary

The two graphs above summarize Terravest’s acquisition activity under this leadership team. Terravest’s major deal in 2014 was its purchase of Jericho, a Quebec-based home heating tank manufacturer purchased from Clarke and Charles Pellerin, who at the time was Jericho’s Executive Chairman, for $36 million. Almost one third of the consideration for Jericho was in the form of Terravest stock and warrants. Clarke took their entire consideration in seller notes whereas Pellerin was paid entirely in Terravest equity. Pellerin has held executive leadership positions and a significant ownership stake in Terravest since then. And the shares he was paid with would end up being the last issued as acquisition consideration until 2021.