Carrier's Gift

Analyzing and Forecasting Watsco's Acquisition Activity

In the wake of the Global Financial Crisis, Watsco nearly doubled the size of their business by forming three joint ventures with Carrier. My goal in this short write-up is to:

Analyze the Carrier joint ventures

Analyze more recent acquisition activity

Forecast contributions of future activity to both Watsco’s results and shareholder returns

In their 2009 annual report, United Technologies shared,

…as part of it’s business transformation strategy, Carrier completed divestitures of several lower-margin businesses, acquired several higher margin service businesses, and formed…Carrier Enterprise, LLC, a venture with Watsco, Inc. to distribute Carrier, Bryant, Payne and Totaline residential and light commercial HVAC products in the U.S. sunbelt region and selected territories in the Caribbean and Latin American

Watsco’s CEO, Al Nahmad remarked,

This is a blockbuster event for our Company as we are almost doubling our size and scale in the marketplace

Nahmad continued,

We see a substantial opportunity to expand Carrier Enterprises historical operating margin…As part of Watsco, Carrier Enterprises locations will have the opportunity to sell additional parts, supplies and other complementary accessories through its existing operating structure, leveraging existing customer relationships and costs…Carrier Enterprise will operate on a decentralized basis and continue to be led by its existing management team…Watsco’s talent base is significantly expanded

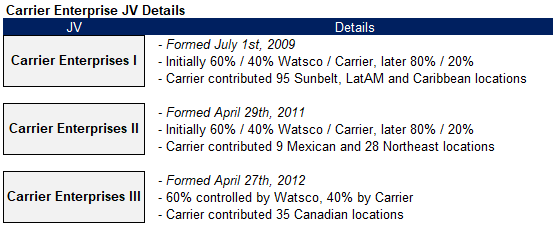

From 2009 to 2012 Watsco formed two more joint ventures with Carrier;

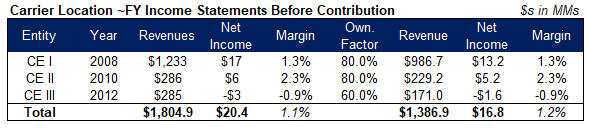

To answer whether Watsco paid a fair price, let’s compare what they paid versus what they received. First, what did Watsco receive? In the 10-Ks released following the JVs, Watsco disclosed what full year and prior year revenues and net income would have been as if each JV began on 1/1 of the year before their consummations, allowing us to isolate the Carrier locations’ contributions. Before going too far, it is worth acknowledging the volatile conditions around this time. Watsco’s net income decreased (18%) in 2007, (11%) in 2008, (15%) in 2009 before growing +117% 2010, +23% in 2011 and 14% in 2012. We know that Carrier was ‘transforming’ it’s business, typically a reaction to poor results as opposed to the other way around.

My best guess is that in the three years before their contribution to the Watsco JVs, the Carrier locations generated $1,804.9mm in sales and $20.4mm in net income. Adjusted for their JV ownerships, Watsco’s share of the the locations results would have been $1,386.9mm in sales and $16.8mm in net income. The three Carrier Enterprises grew Watsco’s consolidated location count +39%, revenues +79% and net income +25% compared to 2007 values. Of course this snapshot is both incomplete, lacking the context a few years worth of P&L would provide as well as obscured having occurred during unusual market conditions during 2008-2012.

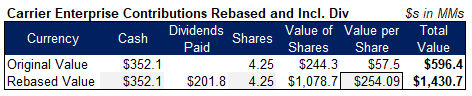

Watsco contributed a total of $596.4mm in value to the three JVs across 7 different transactions using cash, newly issued shares and locations. A simple purchase price multiple over net income, $596.4mm / $16.8mm shows a 35.5x multiple of earnings.

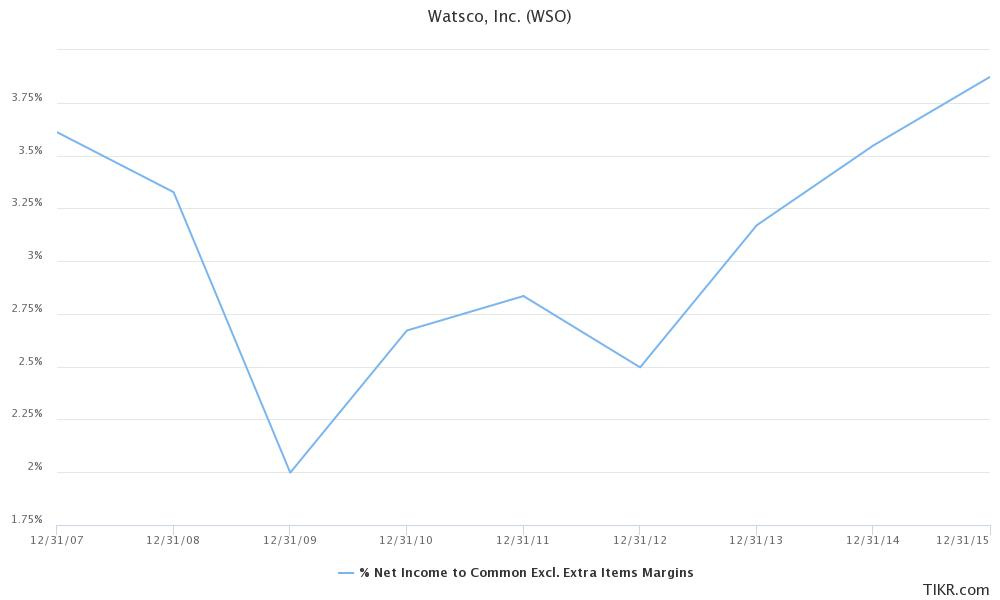

But in the years immediately after forming the JVs, Watsco improved their net income margins by ~30bps per year. One of the reasons why Carrier and Watsco entered into the JVs was to expand each locations product catalogs beyond Carrier equipment, improving 4-wall economics and margins.

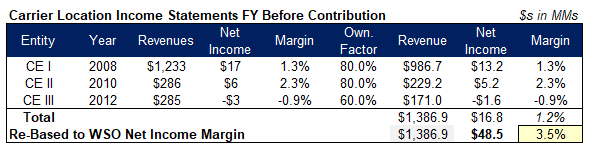

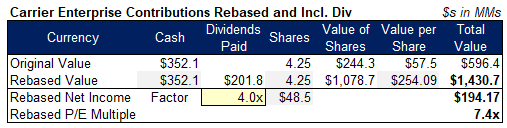

If we assume the Carrier locations achieved 3.5% margins, then Watsco paid $596.4mm for $48.5mm of net income, a 12.3x multiple of net income. But Watsco’s use of shares changes our answer again. Watsco issued a total of 4.25mm shares, of which 94,784 were class B shares (10 votes per share versus 1 vote for each common share). Using the 28.3mm total shares outstanding as at 12/31/2008, Watsco increased their shares outstanding by 15%. Post issuance, Carrier owned 13% of shares and slightly more voting power using 32.4 shares outstanding as at 12/31/2012.

After a fantastic decade for Watsco’s stock, the shares issued as Carrier Enterprise contributions look pricier. Using an updated price per share of $254.09 and acknowledging ~$200mm in dividends paid to the newly issued shares over the decade, Watsco cash and share contributions to the three initial Carrier enterprises are now worth $1,431mm. But from the dates the JVs were formed, Watsco has grown its net income by 4x or 15% compounded annually. If we grow the Carrier Enterprise initial net income by the same factor, the purchase price multiple of net income actually is lower, 7.4x, because Watsco’s net income growth has exceeded that of their shares:

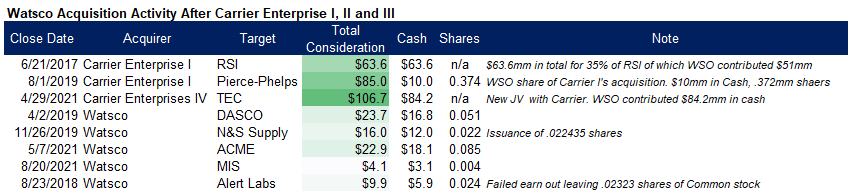

Watsco focused their entirety of their acquisition efforts on Carrier Enterprise I, II and III from 07/2009 when they formed the first JV through 02/2017 when they increased their ownership of CE II to 80%. In 2017, Carrier Enterprise I previewed Watsco’s new acquisition style by announcing their purchase of 35% of Russell Sigler, Inc. (“RSI”) for $63.6mm in cash.

Russell Sigler, Inc., established in 1950, is one of the largest HVAC distributors in North America with annual sales of approximately $650mm…over 10,000 customers from 30 locations throughout Arizona, California, Idaho, New Mexico, Nevada and portions of Texas…Watsco has exclusive rights to purchase ownership interests from current shareholders that may elect to sell in the future

Carrier Enterprise I’s acquisition of 35% of RSI for $63.6mm implies an enterprise value of $181.7mm for RSI. If we assume RSI’s $650mm in sales generated net income of $19.5 / 3.0% margins, than Carrier Enterprise’s purchase price multiple was 9.3x.

After using the JV to purchase RSI in 2017, Watsco again used Carrier Enterprise I to purchase Pierce-Phelps in 8/2019 for $85mm, paid for primarily in WSO shares. If we assume Pierce-Phelps’ sales of $206mm generated $6.2mm in net income (3.0% margin), than Carrier I’s purchase price multiple was 13.8x.

In 2021, Watsco and Carrier formed a fourth JV which they used to purchase Temperature Equipment Control, “TEC” for $106.7mm. If we assume TEC’s $291mm in sales generated $8.7mm in net income (3.0% margin), than CE IV paid a purchase price multiple of 12.3x.

Al Nahmad described TEC as,

one of the most iconic, entrepreneurial, long-standing family businesses in our industry…

and continued,

We look forward to supporting their growth with capital, ideas, technology and our industry relationships to build on their historical success

In contrast to the three large deals done through Carrier JVs, Watsco purchased 5 businesses on their own since 2018 for a total of $76.6mm in value. The pattern is obvious, Watsco and Carrier prefer to invest via their JVs as opposed to return excess capital. Carrier may have gifted Watsco assets 10 years ago, but Watsco has returned the favor via operating results and acquisition activity. While public shareholders have pay high teens multiples for WSO net income, Carrier gets to participate alongside Watsco purchasing businesses for low teens multiples of earnings.

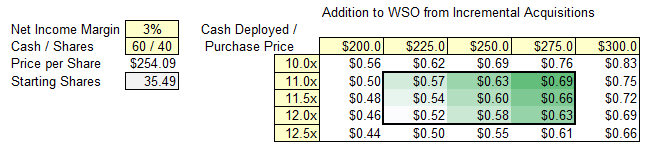

Looking ahead, we can forecast the addition to Watsco’s results from acquisitions by combining CE I’s exclusive rights to purchase the remaining 65% of RSI with a guess at additional M&A activity Watsco and their Carrier JVs may pursue.

Carrier Enterprises I has the exclusive rights to purchase all of the remaining ownership interests in RSI at a specified multiple of earnings, I guess the same 9.3x the first 35% was sold at. If true, buying the remaining ownership of RSI right now would result in $0.29 of additional EPS for Watsco.

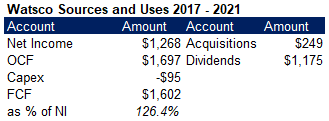

Before forecasting what other acquisition Watsco will accomplish in five years, let’s take a big picture look at sources and uses over their last five fiscal years:

Watsco converted 126% of their $1.3B of net income into $1.6B of free cash flow. Of that $1.6B, $1.2B was paid out as dividends to shareholders while only 15% of FCF, $249 was used for acquisitions. My point is that Watsco’s acquisition activity is limited by their opportunity set. Acquisitions are the end results of original owners finally deciding to sell and calling Watsco likely after decades of contact. My analysis below assumes that Watsco buys businesses that generate 3.0% net income margins, slightly worse than Watsco. I also assume transactions will be funded 60% / 40% cash / stock, in-line with 2017 - 2021. I also am showing Watsco’s share of transactions, assuming Carrier Enterprise JVs will continue to be conduits through which Watsco transacts large M&A.

My base case is that Watsco deploys $250mm in cash causing $167mm in new shares to be issued resulting in $0.60 of new EPS over the next five years. More cash deployed at lower multiples could increase new EPS to as much as $0.83. With $0.29 from an eventual purchase of all of RSI, Watsco shareholders may benefit from $0.89 of new EPS, all highly accretive. As a % of Watsco’s LTM EPS of $13.47, $0.89 is a 6.6% increase. Watsco shareholders should not expect more than a percentage point or two benefit to their returns from acquisitions over the coming years unless The Company is able to significantly increase their deployment.